Introduction to Algorithmic Trading Strategies

Algorithmic trading has become a crucial aspect of the financial markets, with many traders and investors relying on sophisticated computer programs to execute trades at high speeds and frequencies. These programs are based on various trading strategies, each with its own strengths and weaknesses. Two popular strategies used in algorithmic trading are mean reversion and momentum strategies. In this article, we will explore the differences between these two strategies, their underlying principles, and how they can be used to optimize trading performance.

Understanding Mean Reversion Strategies

Mean reversion strategies are based on the idea that asset prices tend to revert to their historical means over time. This strategy assumes that if an asset's price deviates significantly from its mean, it will eventually return to its mean. Mean reversion strategies aim to capitalize on this phenomenon by buying undervalued assets and selling overvalued ones. For example, if a stock's price has fallen significantly below its 50-day moving average, a mean reversion strategy might buy the stock, anticipating that its price will revert to its mean.

A key aspect of mean reversion strategies is the use of statistical models to identify undervalued and overvalued assets. These models can include metrics such as the Bollinger Bands, which measure volatility, or the Relative Strength Index (RSI), which measures the magnitude of recent price changes. By using these models, traders can identify potential buying and selling opportunities and execute trades accordingly.

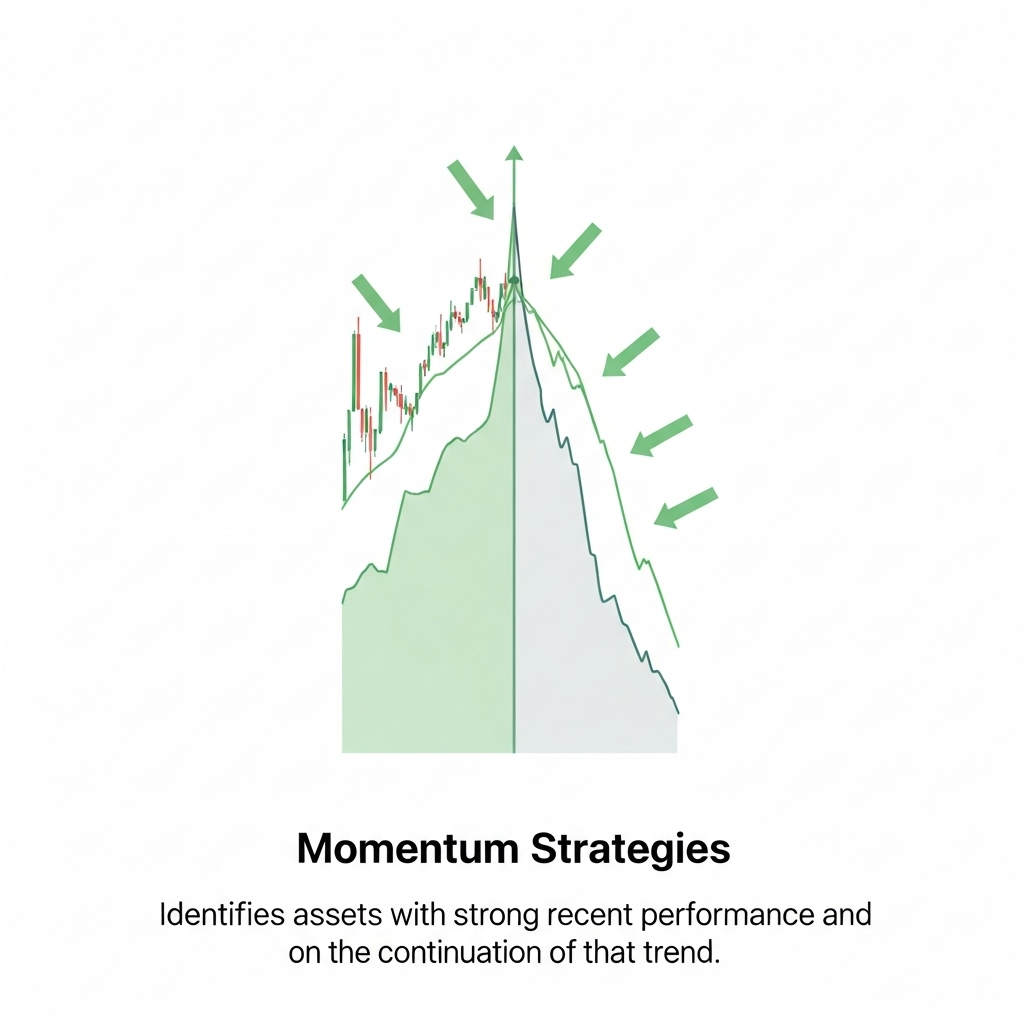

Understanding Momentum Strategies

Momentum strategies, on the other hand, are based on the idea that assets that have performed well in the past will continue to perform well in the future. This strategy assumes that trends in asset prices will persist, and that buying assets with high momentum will result in higher returns. Momentum strategies aim to capitalize on this phenomenon by buying assets with high momentum and selling those with low momentum. For example, if a stock's price has been increasing rapidly over the past few weeks, a momentum strategy might buy the stock, anticipating that its price will continue to rise.

A key aspect of momentum strategies is the use of trend-following indicators, such as moving averages or the Moving Average Convergence Divergence (MACD) indicator. These indicators help traders identify trends in asset prices and execute trades accordingly. Momentum strategies can be further divided into two sub-categories: long-only momentum strategies, which focus on buying assets with high momentum, and long-short momentum strategies, which involve both buying assets with high momentum and selling those with low momentum.

Key Differences Between Mean Reversion and Momentum Strategies

The key difference between mean reversion and momentum strategies lies in their underlying assumptions about asset price behavior. Mean reversion strategies assume that asset prices will revert to their historical means, while momentum strategies assume that trends in asset prices will persist. This difference in assumptions leads to distinct trading behaviors, with mean reversion strategies focusing on buying undervalued assets and selling overvalued ones, and momentum strategies focusing on buying assets with high momentum and selling those with low momentum.

Another key difference between the two strategies is their risk profile. Mean reversion strategies tend to be more conservative, as they aim to capitalize on undervalued assets and avoid overvalued ones. Momentum strategies, on the other hand, can be more aggressive, as they involve buying assets with high momentum and selling those with low momentum. This can result in higher potential returns, but also higher potential losses if the trend reverses.

Example of Mean Reversion Strategy in Action

To illustrate the concept of mean reversion, consider the following example. Suppose we are analyzing a stock that has a 50-day moving average of $50. If the stock's price falls to $40, a mean reversion strategy might buy the stock, anticipating that its price will revert to its mean. If the stock's price then rises to $55, the strategy might sell the stock, locking in a profit. This example illustrates how mean reversion strategies can be used to capitalize on undervalued assets and avoid overvalued ones.

Example of Momentum Strategy in Action

To illustrate the concept of momentum, consider the following example. Suppose we are analyzing a stock that has been increasing in price over the past few weeks. A momentum strategy might buy the stock, anticipating that its price will continue to rise. If the stock's price then continues to increase, the strategy might hold the stock, allowing the profits to accumulate. This example illustrates how momentum strategies can be used to capitalize on trends in asset prices and generate higher returns.

Conclusion

In conclusion, mean reversion and momentum strategies are two popular algorithmic trading strategies used to optimize trading performance. While both strategies have their strengths and weaknesses, they differ in their underlying assumptions about asset price behavior and their trading behaviors. Mean reversion strategies focus on buying undervalued assets and selling overvalued ones, while momentum strategies focus on buying assets with high momentum and selling those with low momentum. By understanding the differences between these two strategies, traders can develop a more informed approach to algorithmic trading and improve their overall trading performance.

Ultimately, the choice between mean reversion and momentum strategies depends on the trader's risk tolerance, investment goals, and market conditions. A combination of both strategies can also be used to create a hybrid approach that balances the benefits of each. As the financial markets continue to evolve, it is essential for traders to stay informed about the latest developments in algorithmic trading and adapt their strategies accordingly to stay ahead of the curve.