Introduction to Understanding Compliance

Compliance is a crucial aspect of any organization, as it ensures that the company operates within the boundaries set by regulatory bodies. In today's fast-paced and ever-evolving business landscape, understanding compliance is more important than ever. With numerous regulatory rules and guidelines in place, it can be overwhelming for companies to navigate and ensure they are meeting all the requirements. In this article, we will delve into the world of compliance, exploring what it entails, its importance, and how companies can effectively navigate regulatory rules and guidelines.

What is Compliance and Why is it Important?

Compliance refers to the process of ensuring that an organization adheres to all relevant laws, regulations, and standards. This includes internal policies and procedures, as well as external rules and guidelines set by regulatory bodies. Compliance is essential for several reasons. Firstly, it helps to prevent legal and financial repercussions that can arise from non-compliance. Secondly, it promotes a culture of integrity and ethics within the organization, which can enhance its reputation and build trust with customers and stakeholders. Finally, compliance ensures that companies operate in a fair and transparent manner, which is critical for maintaining public trust and confidence in the business.

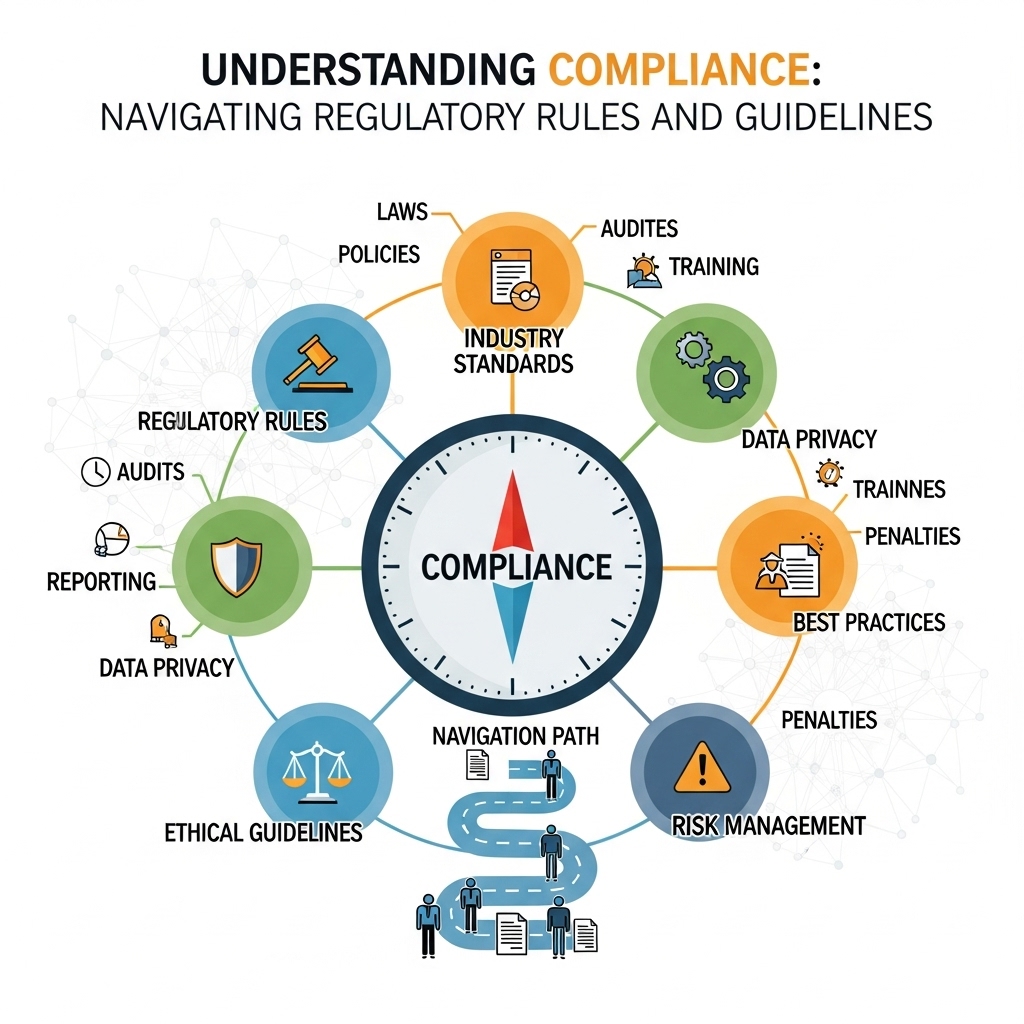

Key Regulatory Rules and Guidelines

There are numerous regulatory rules and guidelines that companies must comply with, depending on their industry, location, and size. Some of the key regulations include the General Data Protection Regulation (GDPR) in the European Union, the Health Insurance Portability and Accountability Act (HIPAA) in the United States, and the Payment Card Industry Data Security Standard (PCI DSS) for companies that handle credit card information. Additionally, companies must also comply with anti-money laundering (AML) and know-your-customer (KYC) regulations, as well as tax laws and employment regulations. For example, a company that operates in the healthcare industry must comply with HIPAA regulations, which require the protection of sensitive patient information. Similarly, a company that handles credit card information must comply with PCI DSS regulations, which require the implementation of robust security measures to protect customer data.

Navigating Regulatory Rules and Guidelines

Navigating regulatory rules and guidelines can be complex and time-consuming, especially for small and medium-sized enterprises (SMEs). To ensure compliance, companies can take several steps. Firstly, they can conduct a thorough risk assessment to identify potential compliance risks and develop strategies to mitigate them. Secondly, they can implement robust policies and procedures that are designed to ensure compliance with relevant regulations. Thirdly, they can provide training to employees on compliance issues and ensure that they understand their roles and responsibilities in maintaining compliance. Finally, companies can engage with regulatory bodies and seek guidance on compliance issues, which can help to prevent misunderstandings and ensure that they are meeting all the requirements. For instance, a company can engage with a compliance consultant who can provide guidance on regulatory requirements and help to develop policies and procedures that ensure compliance.

Best Practices for Ensuring Compliance

To ensure compliance, companies can adopt several best practices. Firstly, they can establish a compliance program that is designed to ensure compliance with relevant regulations. Secondly, they can appoint a compliance officer who is responsible for overseeing compliance issues and ensuring that the company is meeting all the requirements. Thirdly, they can implement a system of internal controls that are designed to prevent non-compliance and detect any compliance issues that may arise. Finally, companies can conduct regular audits and risk assessments to identify potential compliance risks and develop strategies to mitigate them. For example, a company can implement a compliance software that helps to track and manage compliance issues, as well as provide training to employees on compliance issues.

Consequences of Non-Compliance

The consequences of non-compliance can be severe and far-reaching. Companies that fail to comply with regulatory rules and guidelines can face legal and financial repercussions, including fines, penalties, and reputational damage. Additionally, non-compliance can also lead to a loss of public trust and confidence in the business, which can have long-term consequences for the company's reputation and bottom line. For instance, a company that fails to comply with data protection regulations can face significant fines and reputational damage, as well as legal action from affected customers. Similarly, a company that fails to comply with employment regulations can face legal action from employees and reputational damage, which can make it difficult to attract and retain top talent.

Conclusion

In conclusion, understanding compliance is critical for companies that want to operate in a fair and transparent manner. By navigating regulatory rules and guidelines, companies can ensure that they are meeting all the requirements and avoiding the consequences of non-compliance. To ensure compliance, companies can adopt best practices such as establishing a compliance program, appointing a compliance officer, implementing internal controls, and conducting regular audits and risk assessments. By taking a proactive approach to compliance, companies can promote a culture of integrity and ethics, enhance their reputation, and build trust with customers and stakeholders. Ultimately, compliance is an ongoing process that requires continuous monitoring and evaluation, and companies that prioritize compliance can reap significant benefits and avoid the consequences of non-compliance.